The Citation Economy: Which Sources AI Engines Cite, and What That Means for Where You Invest

.png)

The goal is not merely to be listed. It is to be the source the model leans on when it writes the sentence a buyer reads, and that requires earned authority to get selected plus structural clarity to get absorbed. Earned media gets you into that pool. Extractable, evidence-dense content decides whether you get quoted once you are there.

When someone asks ChatGPT which project management tool to buy, or asks Perplexity whether a brand is any good, the model does not reach into a ranked list of ten links.

It assembles an answer from a small set of sources it trusts enough to reference, and the brands named in that answer are the ones that exist, for that buyer, in that moment.

Everything else is invisible.

The set of sources an engine pulls from is a kind of marketplace, with a limited supply of slots, a crowd of brands competing for them, and a currency that decides who gets in.

But it’s not a currency we’ve spent the last decade accumulating.

The Concentration Paradox

The first thing to understand about the citation economy is that it is concentrated and diffuse at the same time.

At the very top, the concentration is extreme.

In its 2026 AI Platform Citation Source Index, communications firm 5W synthesized six published studies covering more than 680 million citations and citation observations across ChatGPT, Google AI Overviews, Perplexity, Gemini, and Claude.

Its cross-study index estimated that the top 15 domains captured 68% of consolidated AI citation share.

That is a heavier concentration than Google’s PageRank ever produced. A handful of mega-sources, led by Reddit, Forbes, LinkedIn, Wikipedia, and YouTube, anchor a large fraction of every answer the major engines generate.

Below that peak, the citation market becomes far more fragmented.

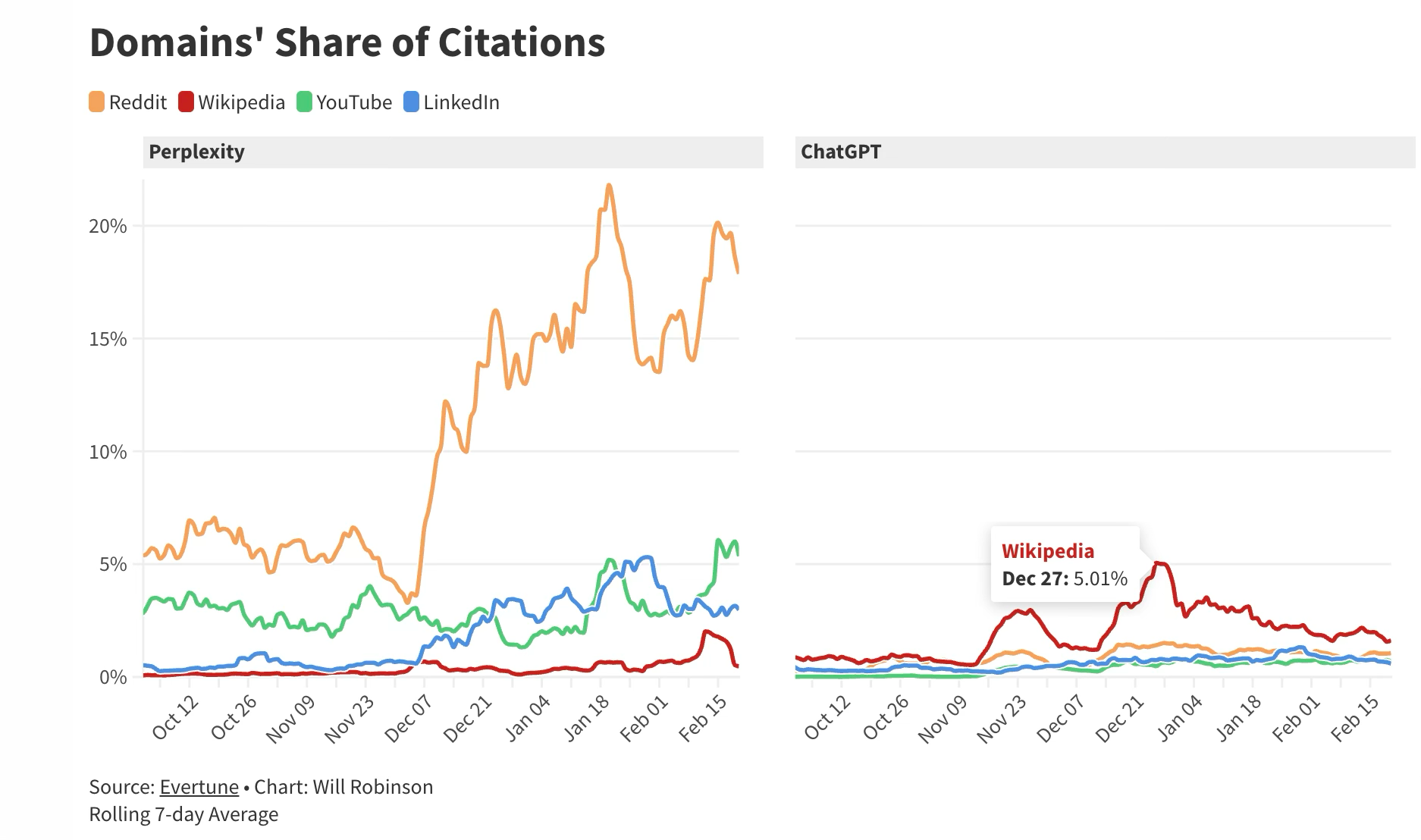

Evertune analysed responses to more than 200 million prompts over five months, focusing on four broadly relevant domains: Reddit, Wikipedia, YouTube, and LinkedIn.

On ChatGPT, Wikipedia was the most frequently cited of the four, but its share topped out at around 5%. Across ChatGPT, Gemini, Google AI Overviews, and Google AI Mode, the four domains combined rarely accounted for more than 5% of citations. The remainder was distributed across thousands of other websites.

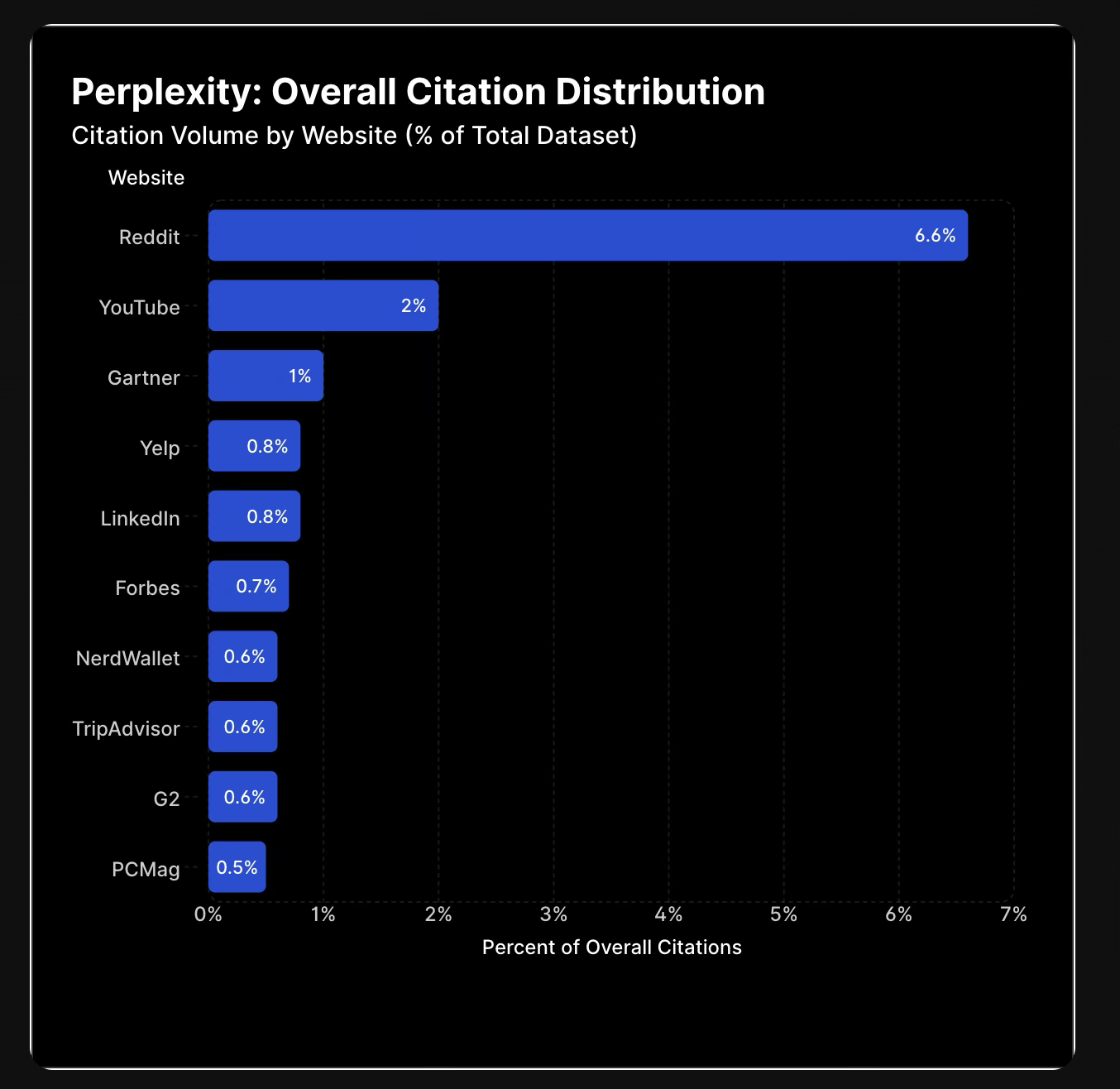

Perplexity was the clear exception. At points during January and February 2026, Reddit appeared in 20% or more of its responses, showing that individual platforms can still develop strong and temporary preferences for particular sources.

The pattern here goes back to my earlier statement that “it is concentrated and diffuse at the same time.”

It is concentrated around a small number of highly influential sources, then quickly becomes long-tailed, platform-specific, and category-dependent.

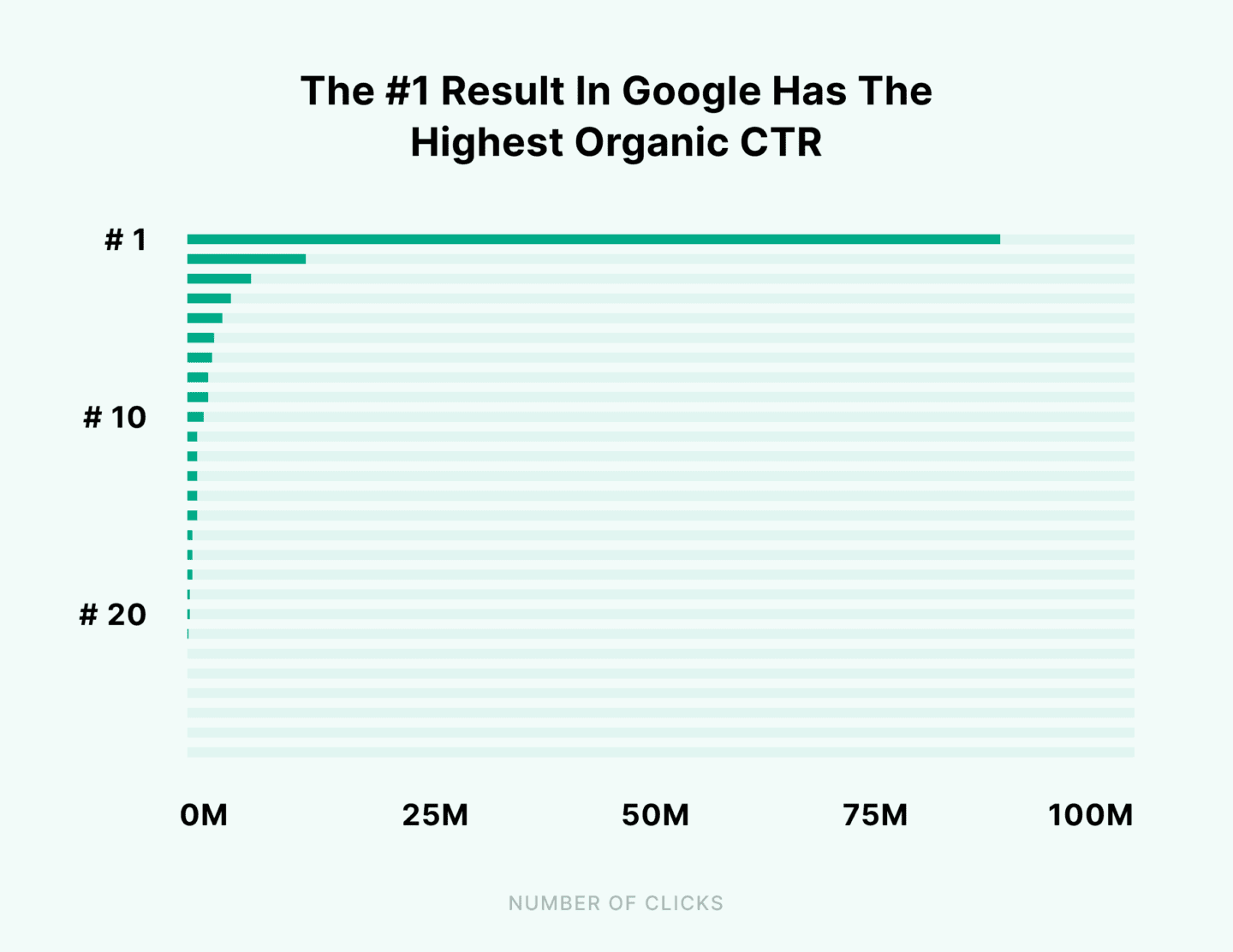

That differs from traditional search, where attention was strongly tied to rank.

Backlinko’s analysis of roughly four million Google results found that the first three organic positions captured more than half of all clicks, while the first result received ten times the click-through rate of the tenth.

In AI citations, the distribution is flatter for everyone below the mega-sources, which changes the nature of the opportunity.

You are almost never going to displace Reddit or Wikipedia as a category-level anchor, so the concentration at the top is not where your effort goes.

The winnable game lives in the long tail, in the category-specific sources that AI engines pull when a query gets specific enough. A niche trade publication, a well-regarded review platform, a comparison page that neutrally covers your category — these are the slots a brand can actually contest, and they are where investment pays back.

The Engines Do Not Shop at the Same Stores

Treating “AI search” as one destination is a mistake, because the engines pull from source pools that barely overlap.

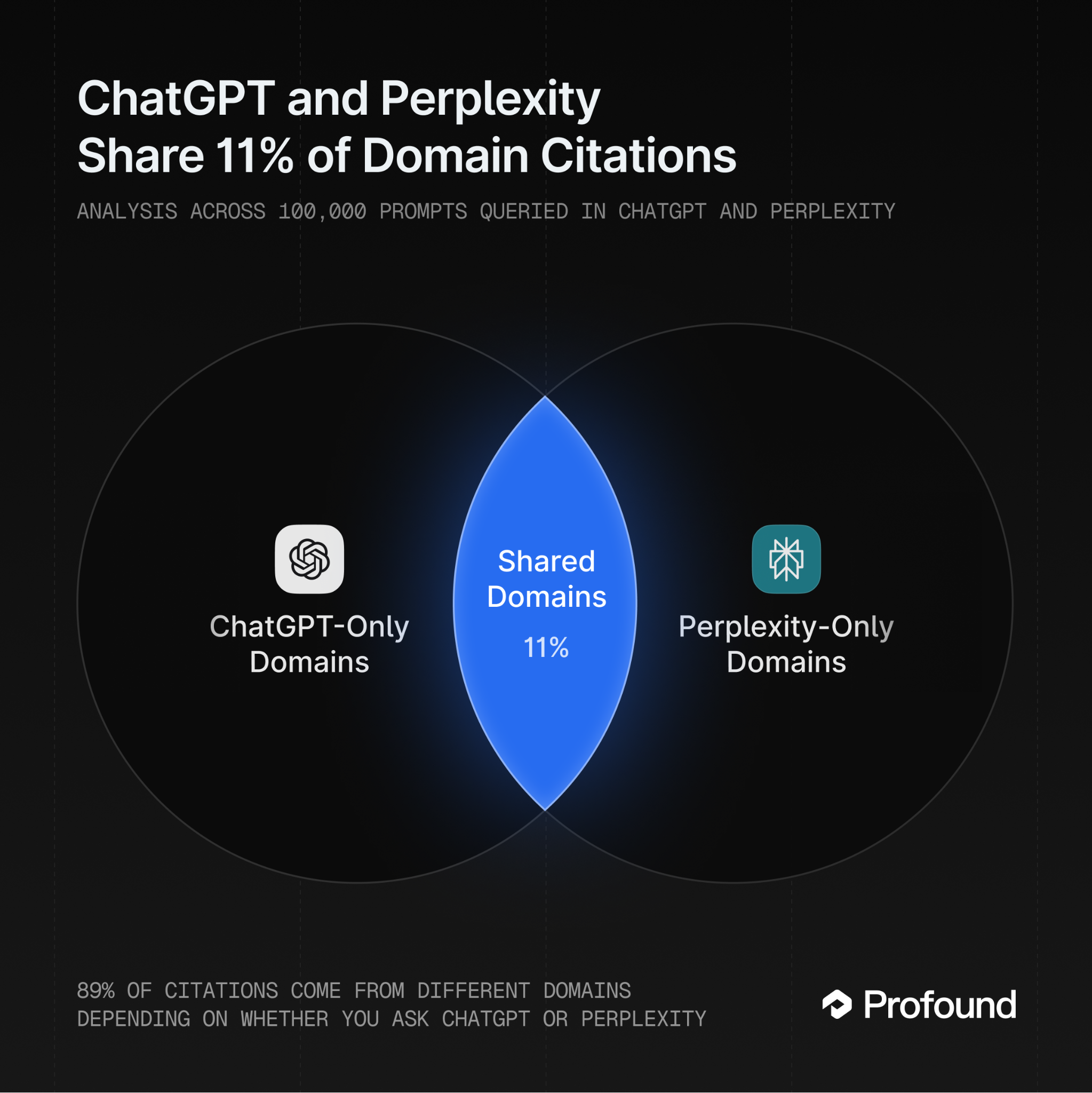

Profound’s study found that only 11% of domains appeared in both ChatGPT’s and Perplexity’s citation sets. The remaining domains appeared exclusively in either ChatGPT or Perplexity.

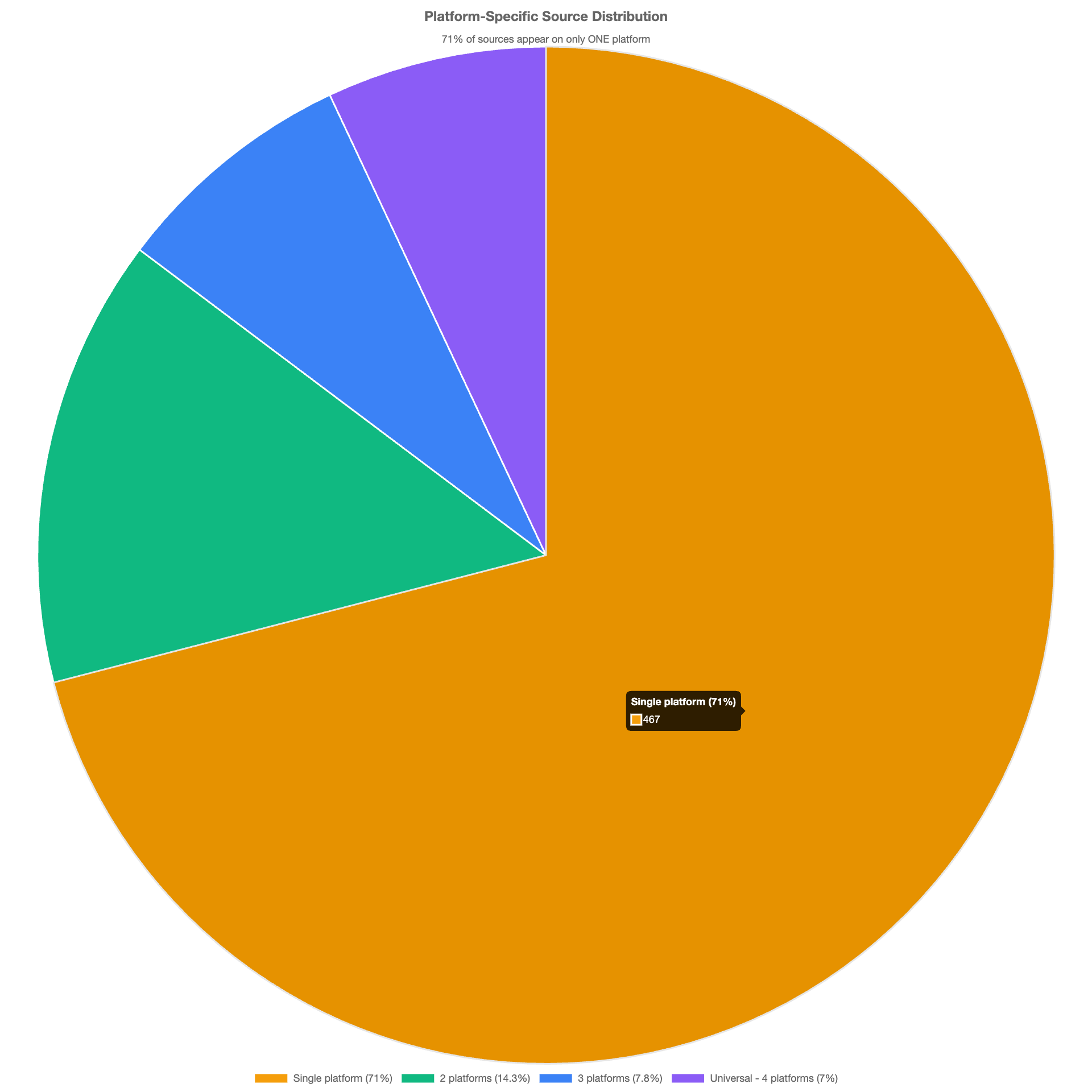

A broader meta-analysis by Dr. Robert Li found the same pattern across ChatGPT, Claude, Perplexity, and Gemini. Of the 467 sources included in the analysis, 71% appeared on only one platform, while just 7% appeared across all four.

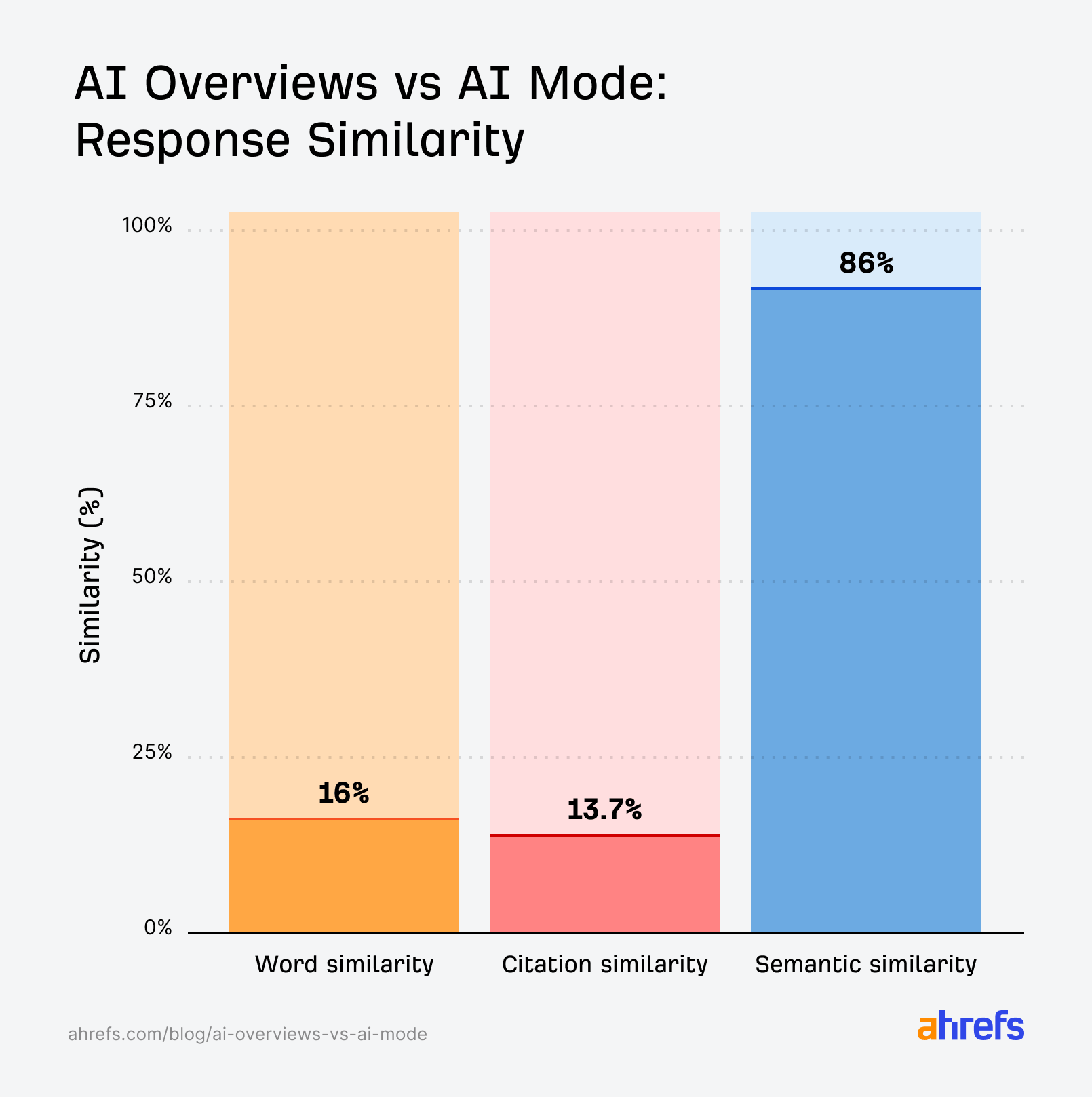

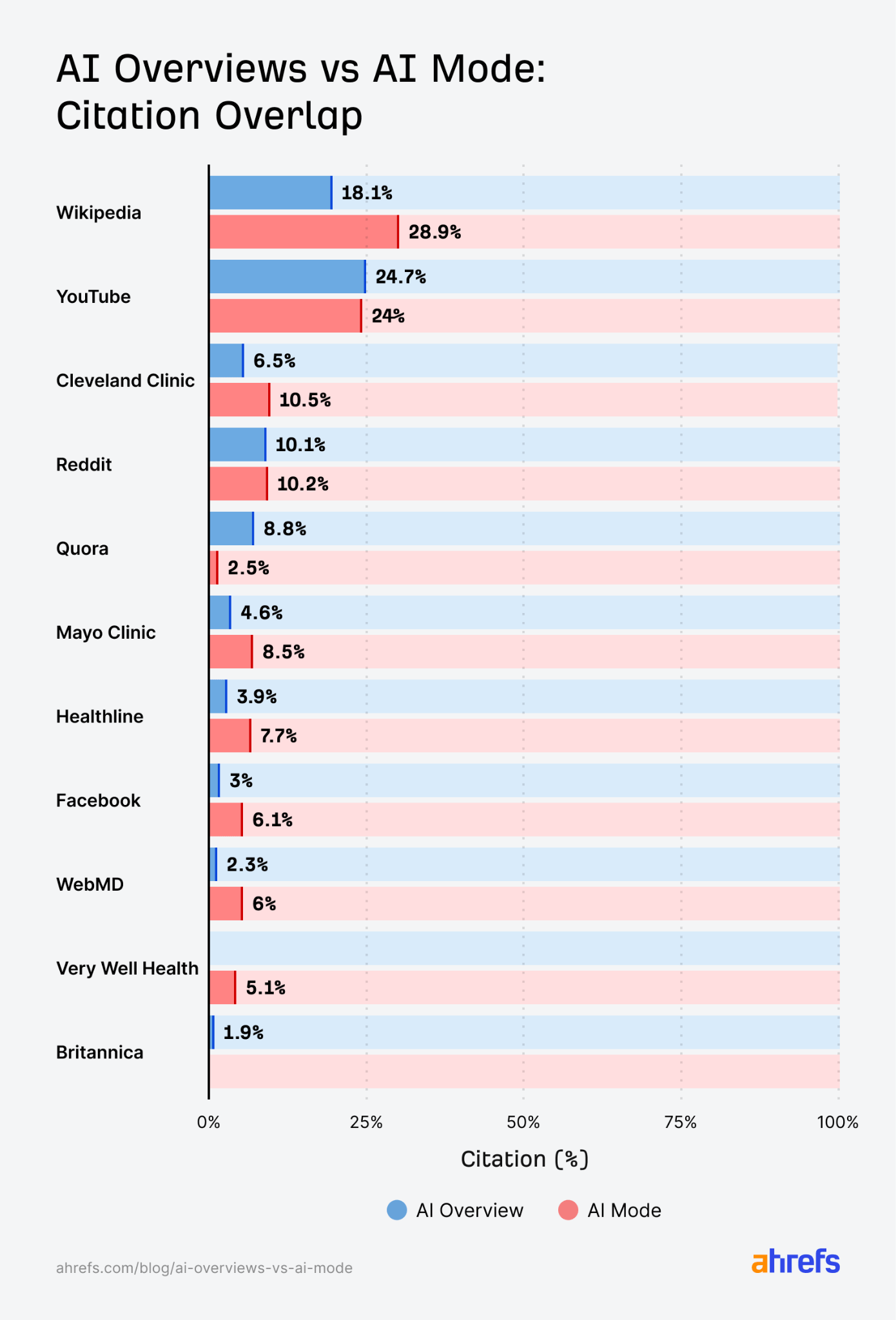

Even Google’s own AI products do not draw from identical source pools. Ahrefs compared 540,000 pairs of AI Overview and AI Mode responses and found that only 13.7% of cited URLs appeared in both. Yet the answers had an average semantic similarity of 86%.

In other words, the two systems usually reached similar conclusions while citing different pages to support them.

The exact overlap rate changes depending on the prompts, platforms, timeframe, and whether a study compares domains or individual URLs. But the direction is consistent—i.e., visibility in one engine does not reliably transfer to another.

The differences also extend to the types of sources each engine trusts.

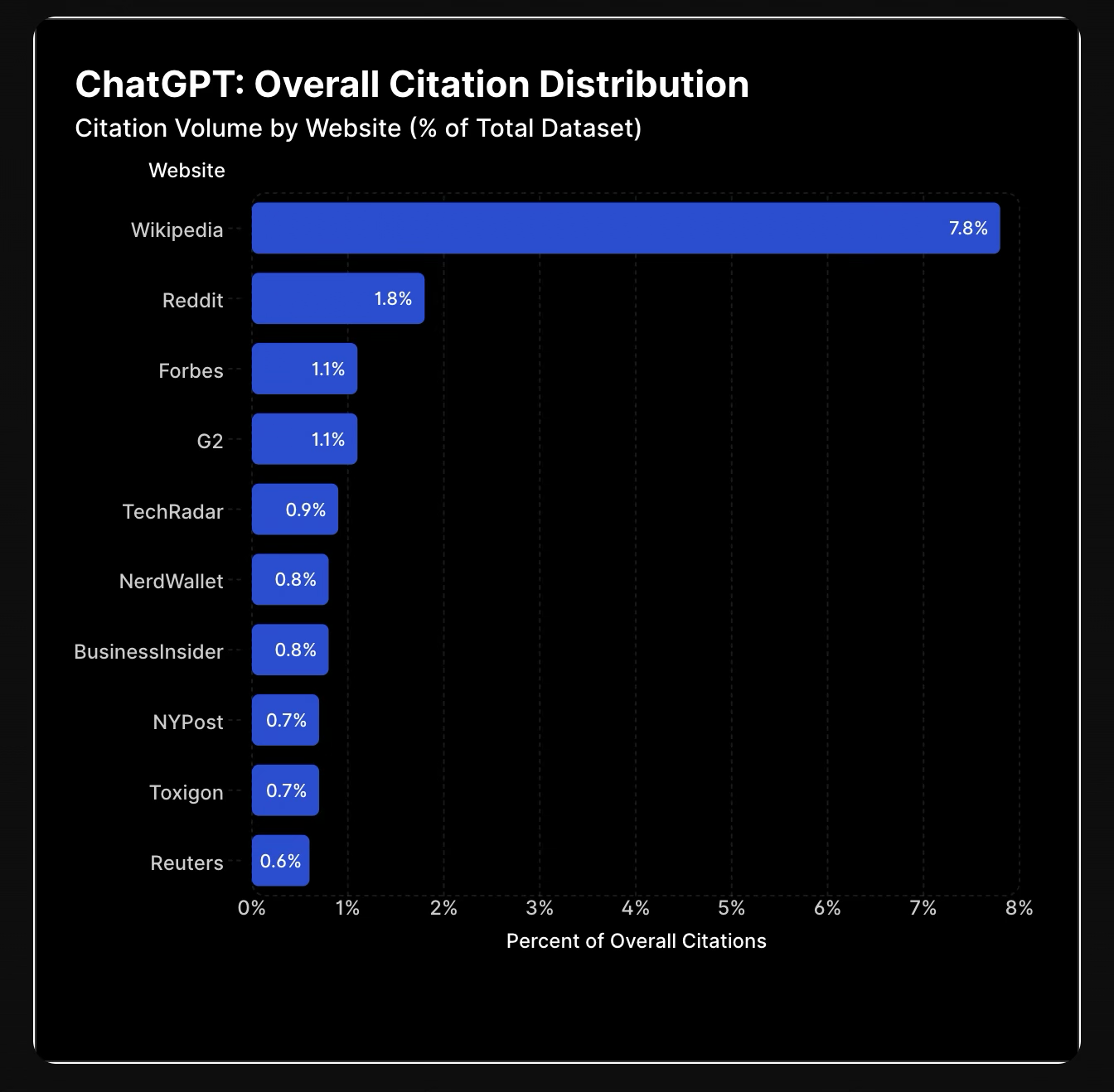

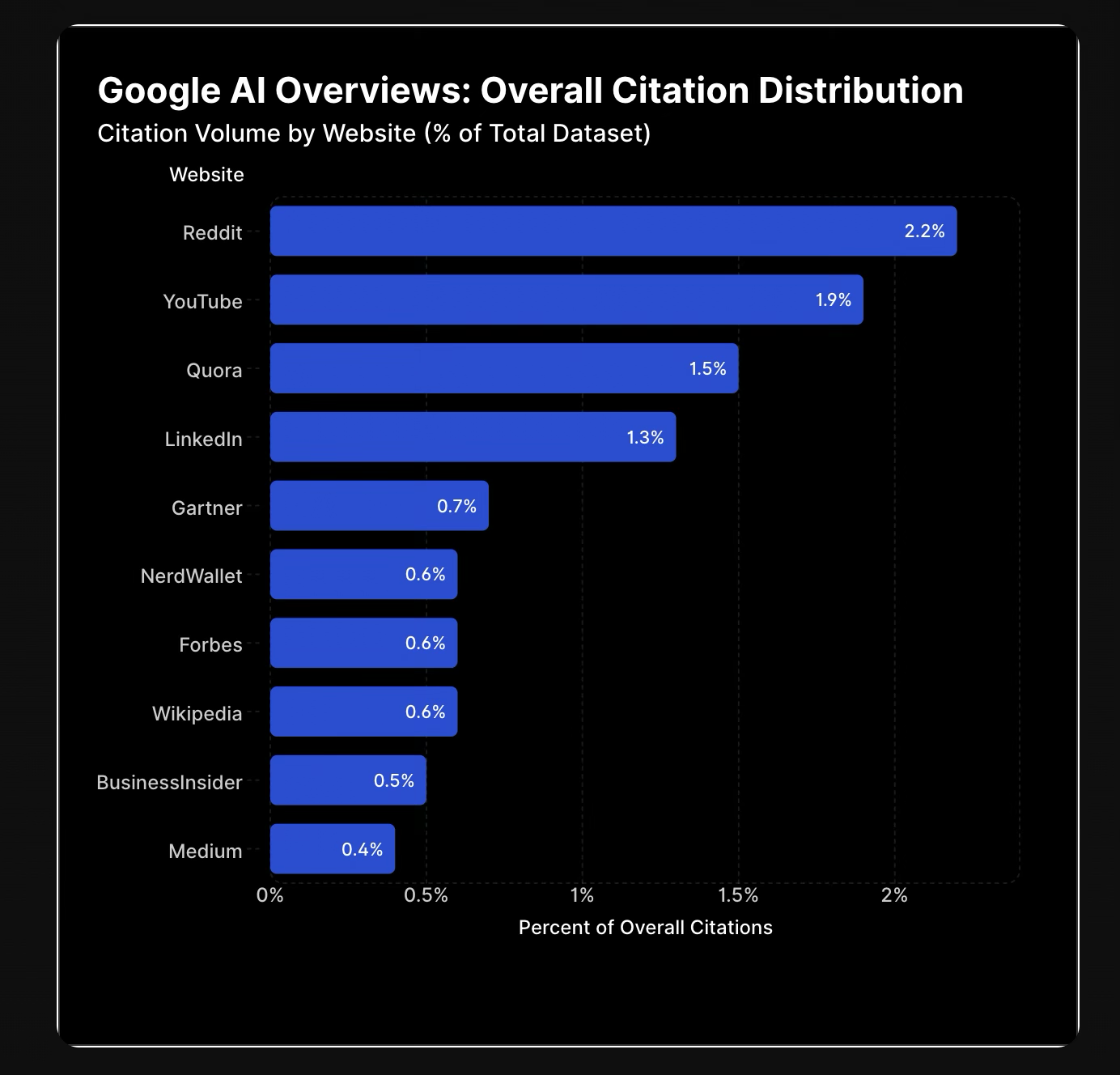

Across Profound’s dataset of 680 million citations, Wikipedia was ChatGPT’s leading source, accounting for 7.8% of all citations. Reddit led Perplexity at 6.6% and Google AI Overviews at 2.2%.

Within each engine’s ten most-cited domains, Wikipedia represented 47.9% of ChatGPT’s citations, while Reddit represented 46.7% of Perplexity’s. Those percentages refer only to citations within the top-ten source groups, not to all citations generated by each platform.

Google’s products also show different preferences. Ahrefs found that YouTube held the top citation position in AI Overviews, while Wikipedia appeared more frequently in AI Mode. AI Overviews also cited videos and core website pages almost twice as often as AI Mode, even though both systems predominantly cited article-format content.

The Consequence

A brand can perform strongly in one engine and remain almost invisible in another.

Slate HQ analysed more than 300,000 citations across six B2B SaaS brands, six AI platforms, and a 90-day period. When it separated the results by platform, the citation profiles for the same brand and content library were so different that they could have belonged to different companies.

The size of the gap varied by company. In Slate’s examples, the difference between a brand’s strongest platform and its ChatGPT visibility ranged from 5x to 71x. One brand had 10% visibility in Google AI Mode but only 0.14% in ChatGPT.

That makes a single, blended “AI visibility” score misleading. It can hide the fact that a brand dominates one citation ecosystem while barely appearing in another.

The implication for the citation economy is that there is no single market to win. There are four or five different markets, each with its own preferred suppliers.

The Inversion That Reverses SEO’s Instincts

The largest and most consequential finding in the citation economy is about who gets cited, and it runs against everything content marketing was built to do.

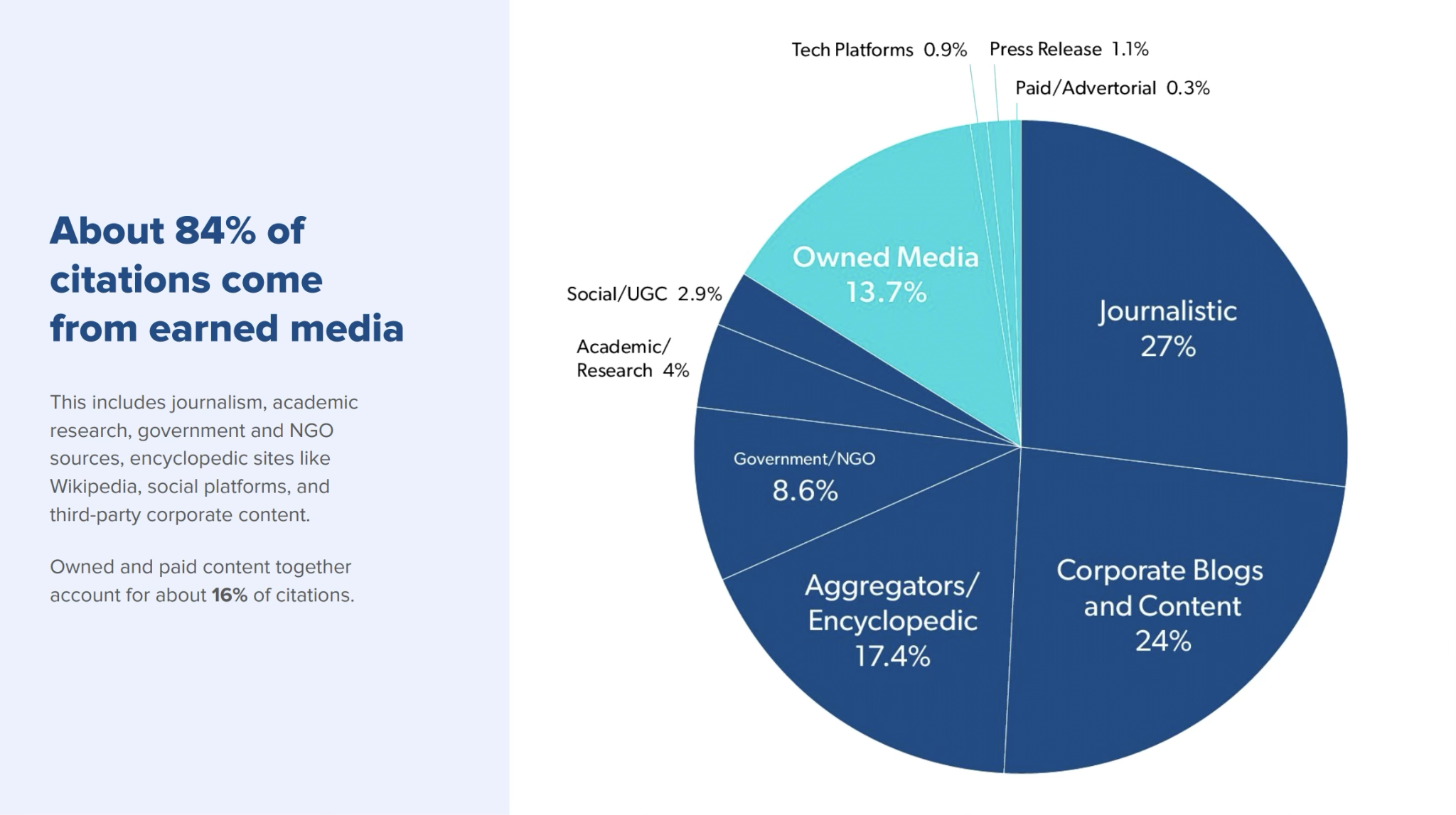

AI engines overwhelmingly cite what other people publish about a brand rather than what the brand publishes about itself. The numbers are consistent across measurement approaches that have nothing else in common.

Muck Rack, analyzing over 25 million cited links from ChatGPT, Claude and Gemini across seventeen industries put earned media at 84% of all citations.

McKinsey’s data pegged a brand’s own website at only 5 to 10% of what AI search references.

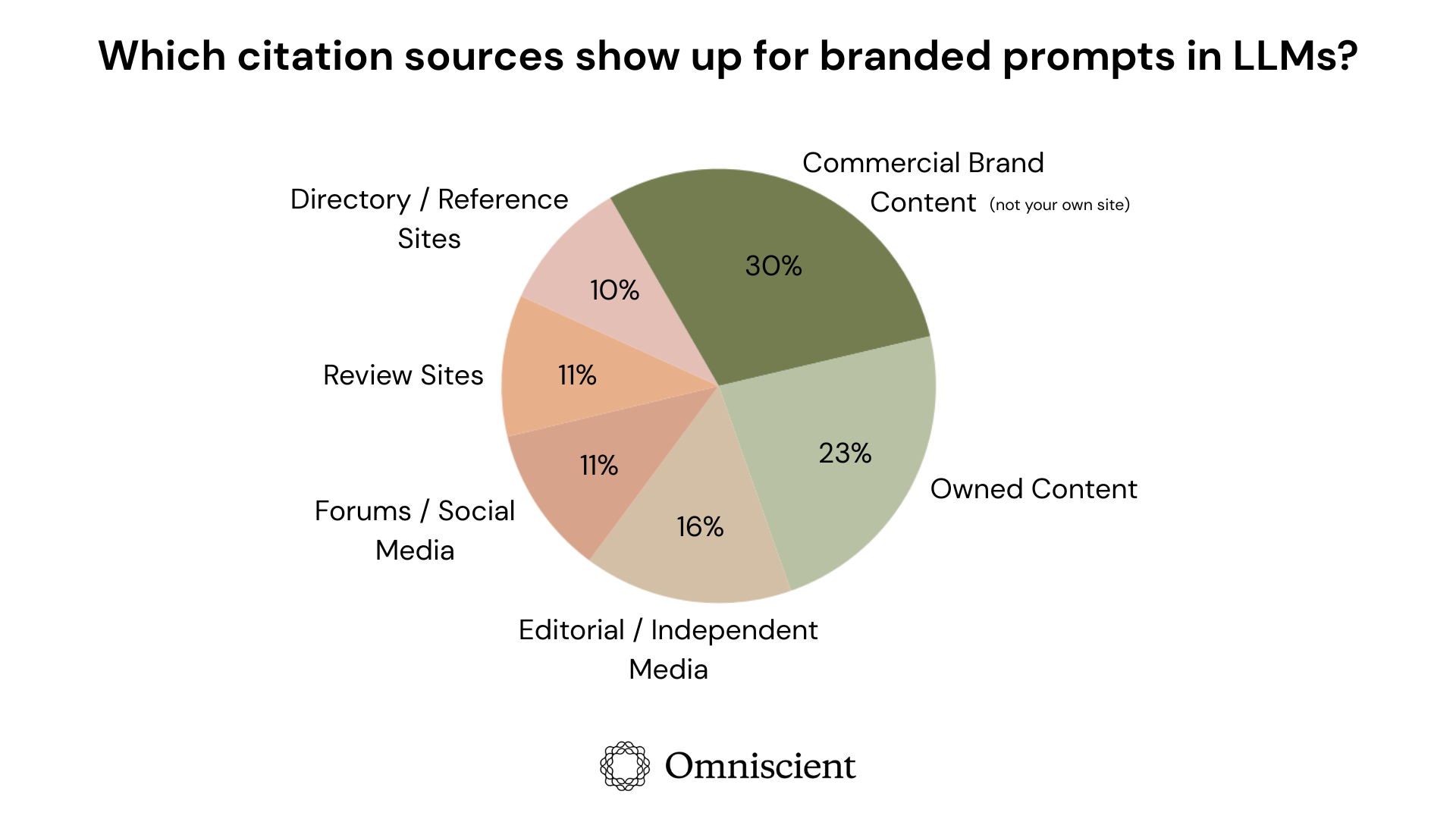

In another study, Cate Dombrowski of Omniscient Digital ran 240 branded prompts through multiple engines and analyzed the resulting 23,387 citations. She discovered that for branded queries, earned media accounted for 48% of citations, commercial third-party content for 30%, and the brand’s own content for just 23%.

What makes this more than a pattern is that a controlled academic study found it to be built into how the systems work.

A University of Toronto team concluded that AI search exhibits a systematic and overwhelming preference for earned media over brand-owned and social content.

Large language models learned what credibility looks like from training data weighted toward editorially independent sources with fact-checking and track records.

When a model assembles an answer, it applies the same weighting, and brand-owned content carries an inherent discount because self-interest is legible to the system.

A news outlet covering a brand provides corroboration, which is harder to manufacture at scale and carries a different status than a company describing itself.

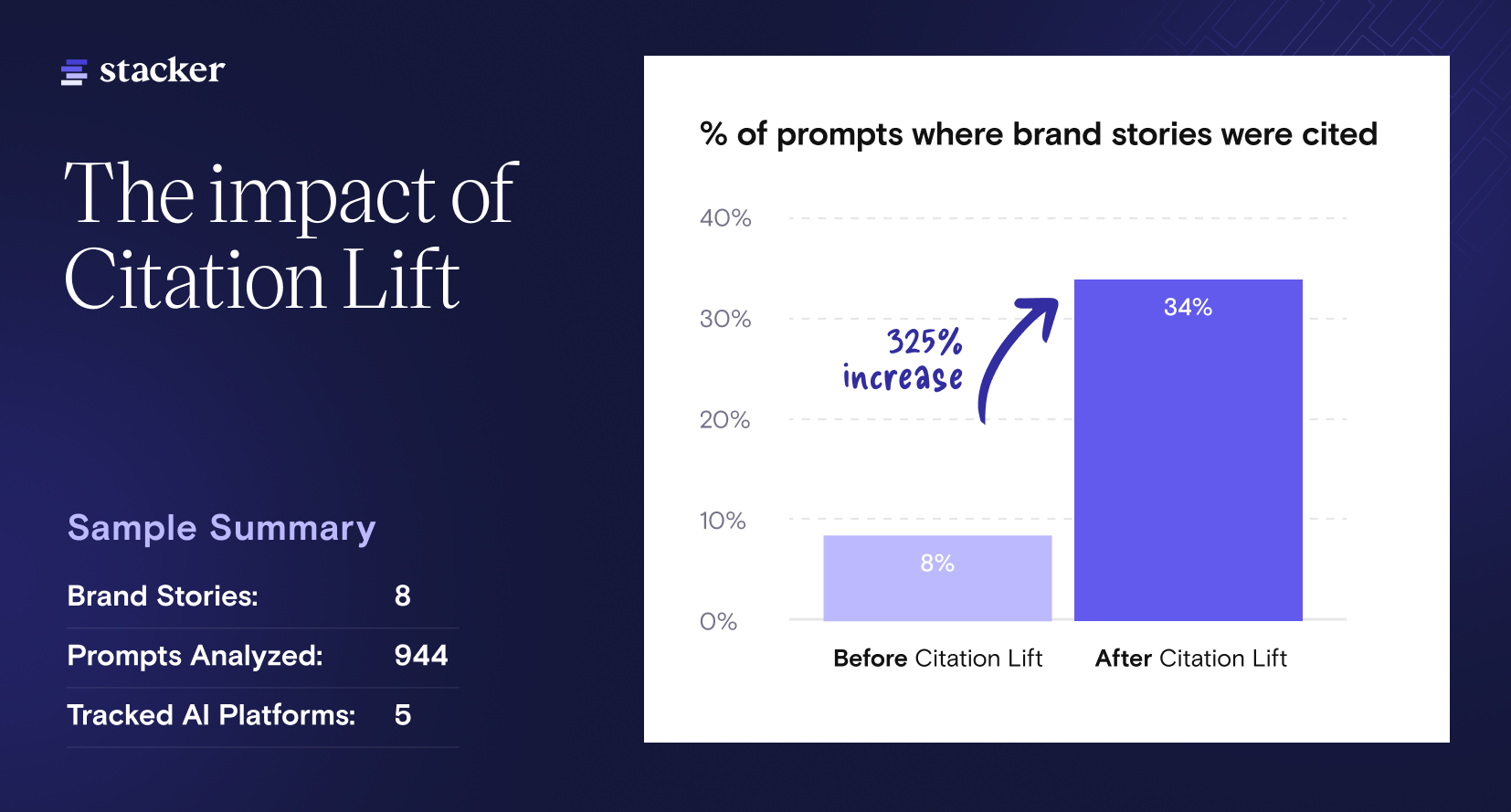

The size of the effect has been measured directly. Stacker and Scrunch ran a controlled experiment across 944 prompt-platform combinations and found that the same article, distributed through third-party news outlets, jumped from an 8% citation rate to 34%.

The variable was not content quality, since the content was identical. It was distribution context because the engines weight the authority of the domain doing the citing.

Going back to McKinsey’s data, if the brand’s own website accounts for something like 5 to 10% of AI citations, then a team that has invested almost entirely in SEO and owned content has optimized for the small channel while leaving the large one untouched.

The One Owned Asset That Still Wins

There is one clear exception to the broader earned-media pattern. And that is original research published on a brand’s own domain.

Generic blog posts and product pages usually repeat information available elsewhere.

However, proprietary research gives an engine evidence that originated with the brand. That does not guarantee a citation, but it gives the engine a direct reason to attribute the page rather than replace it with an equivalent third-party source.

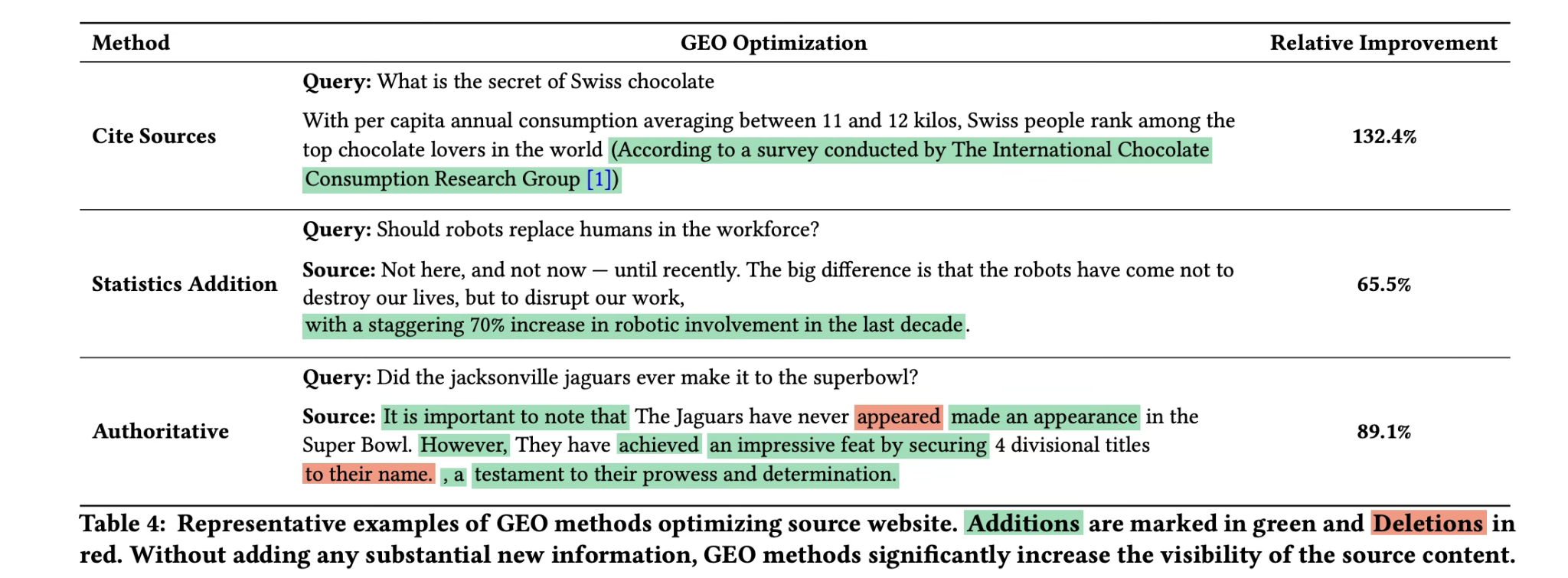

The strongest evidence comes from the original GEO study by researchers from Princeton, Georgia Tech, the Allen Institute for AI, and IIT Delhi.

Using a benchmark of 10,000 queries, the researchers tested how changes to source content affected its visibility in generated answers. Adding statistics, credible quotations, and source citations produced relative improvements of 30% to 40% on the study’s position-adjusted visibility metric and 15% to 30% on its subjective impression metric.

Note: The study tested content that had already been placed within the engine’s available source set. It shows that verifiable facts can increase how prominently a source is used within an answer, not that publishing statistics automatically causes a page to be discovered or cited across the open web.

The Format Economy

Below the question of who publishes the content sits the question of what shape it takes, and here too the engines have clear preferences that reward some formats and quietly starve others.

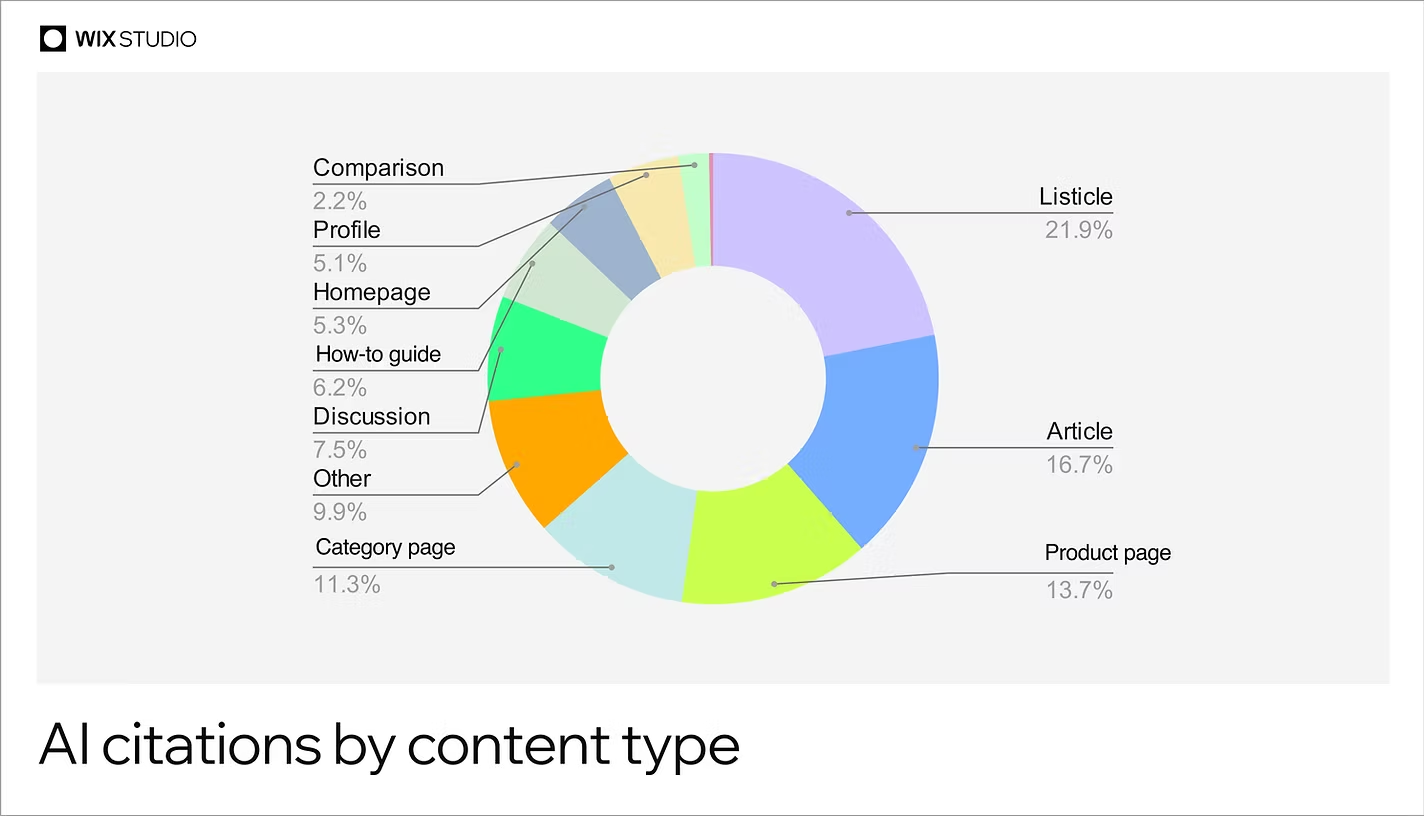

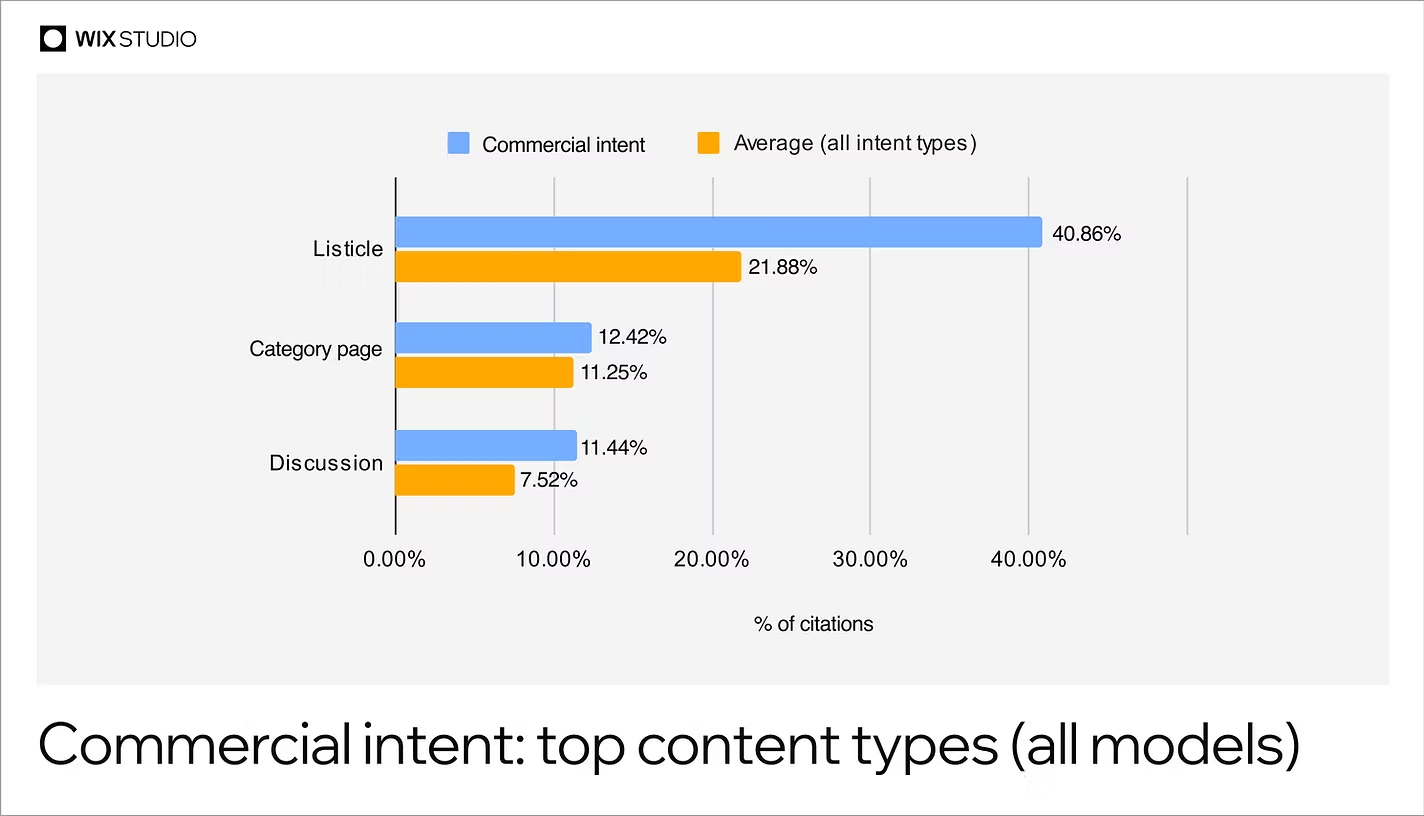

Wix Studio’s AI Search Lab analysed 75,000 answers containing more than one million citations across ChatGPT, Google AI Mode, and Perplexity.

Listicles accounted for 21.9% of citations, articles for 16.7%, and product pages for 13.7%. Together, those three formats generated 52% of all citations in the dataset.

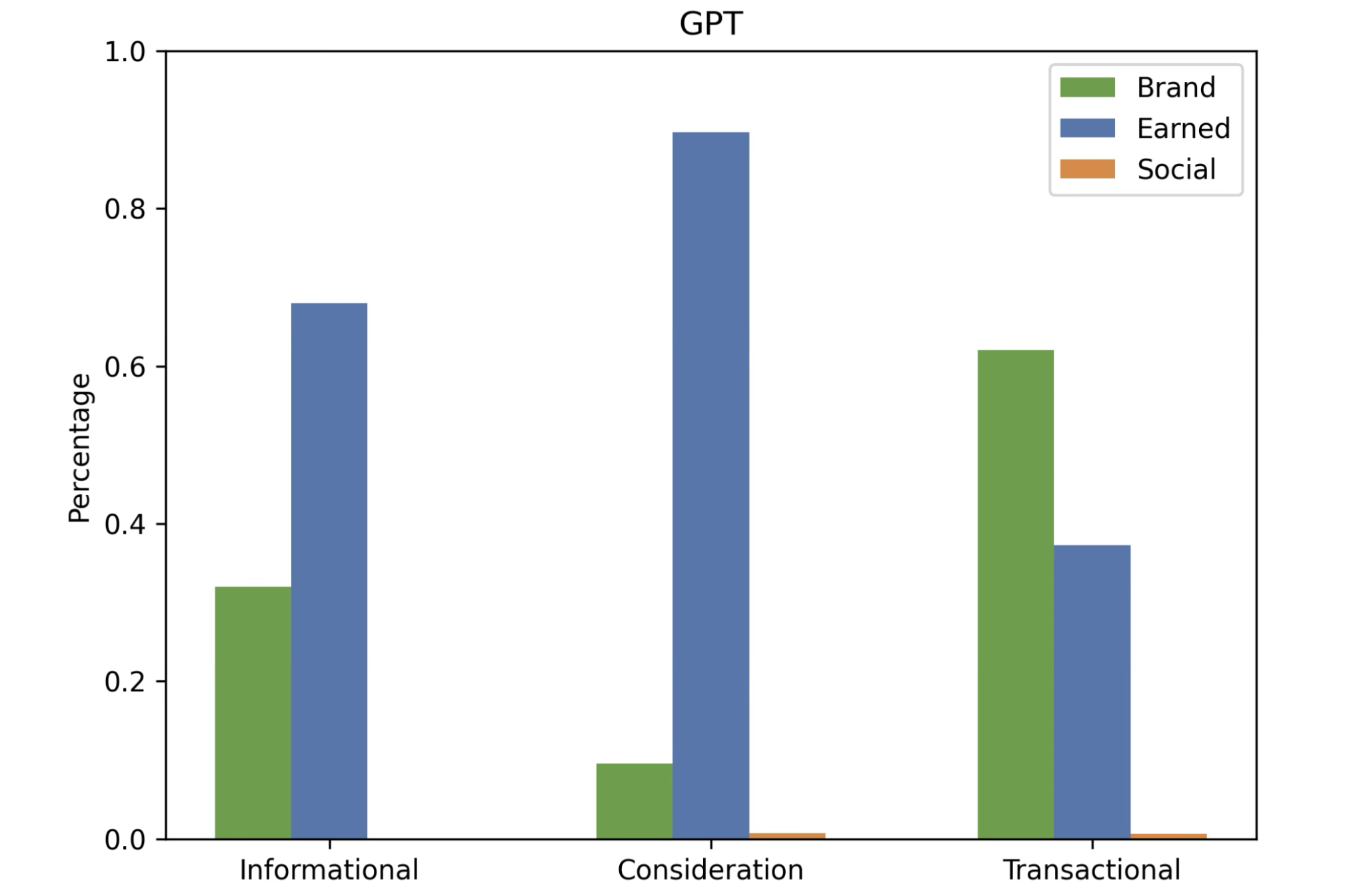

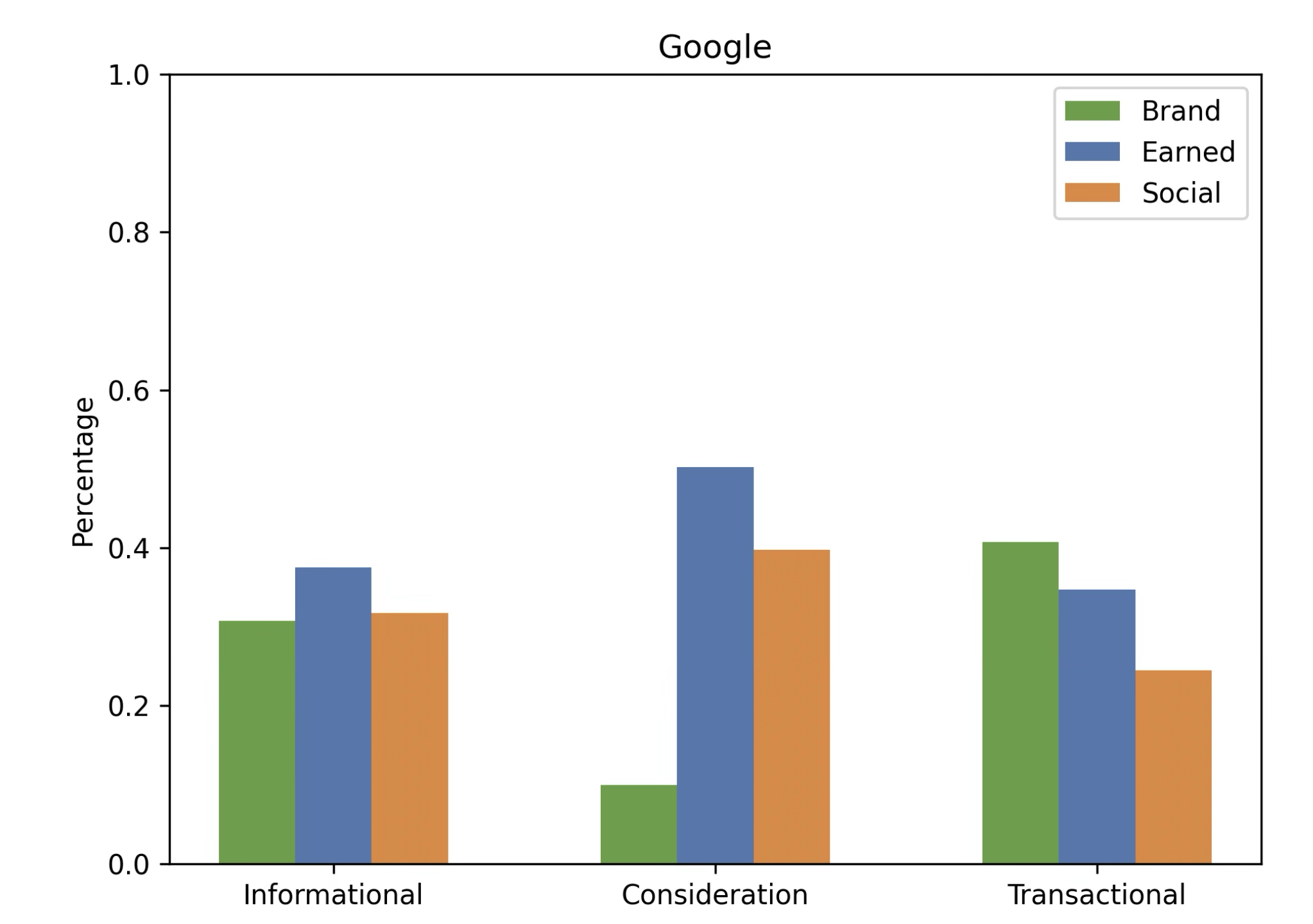

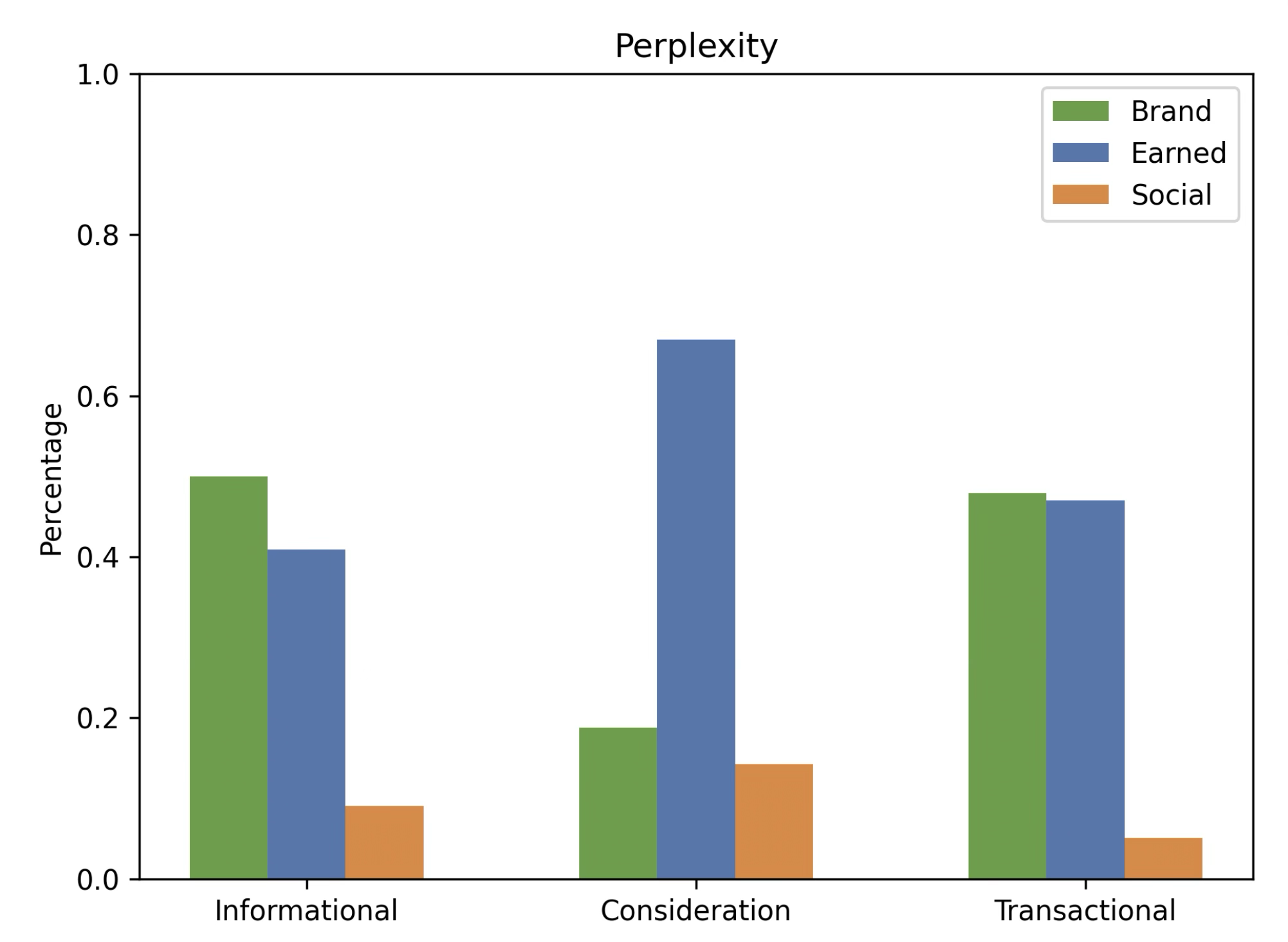

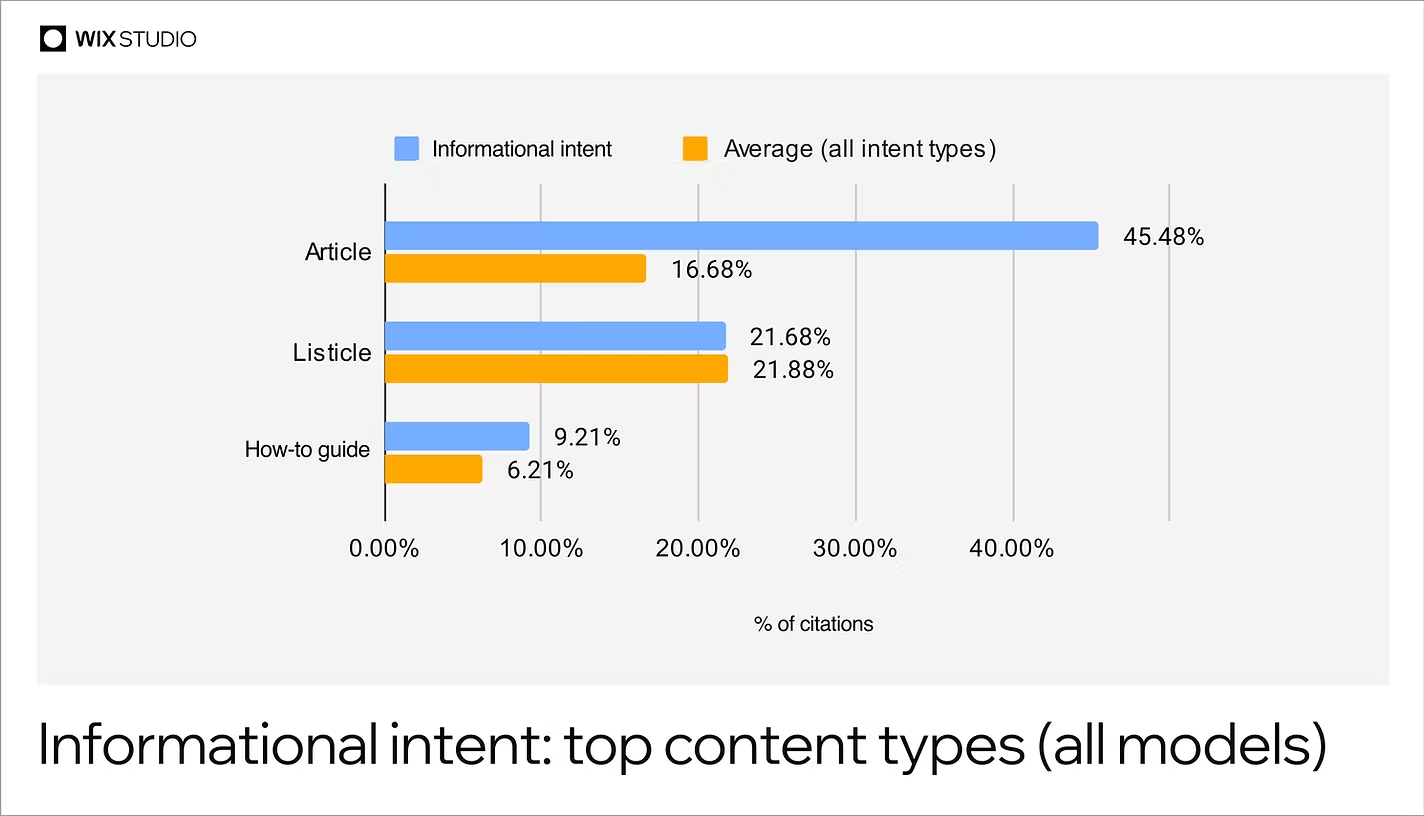

But there was no universally dominant format. Query intent predicted the content type cited more strongly than either the industry or the engine answering.

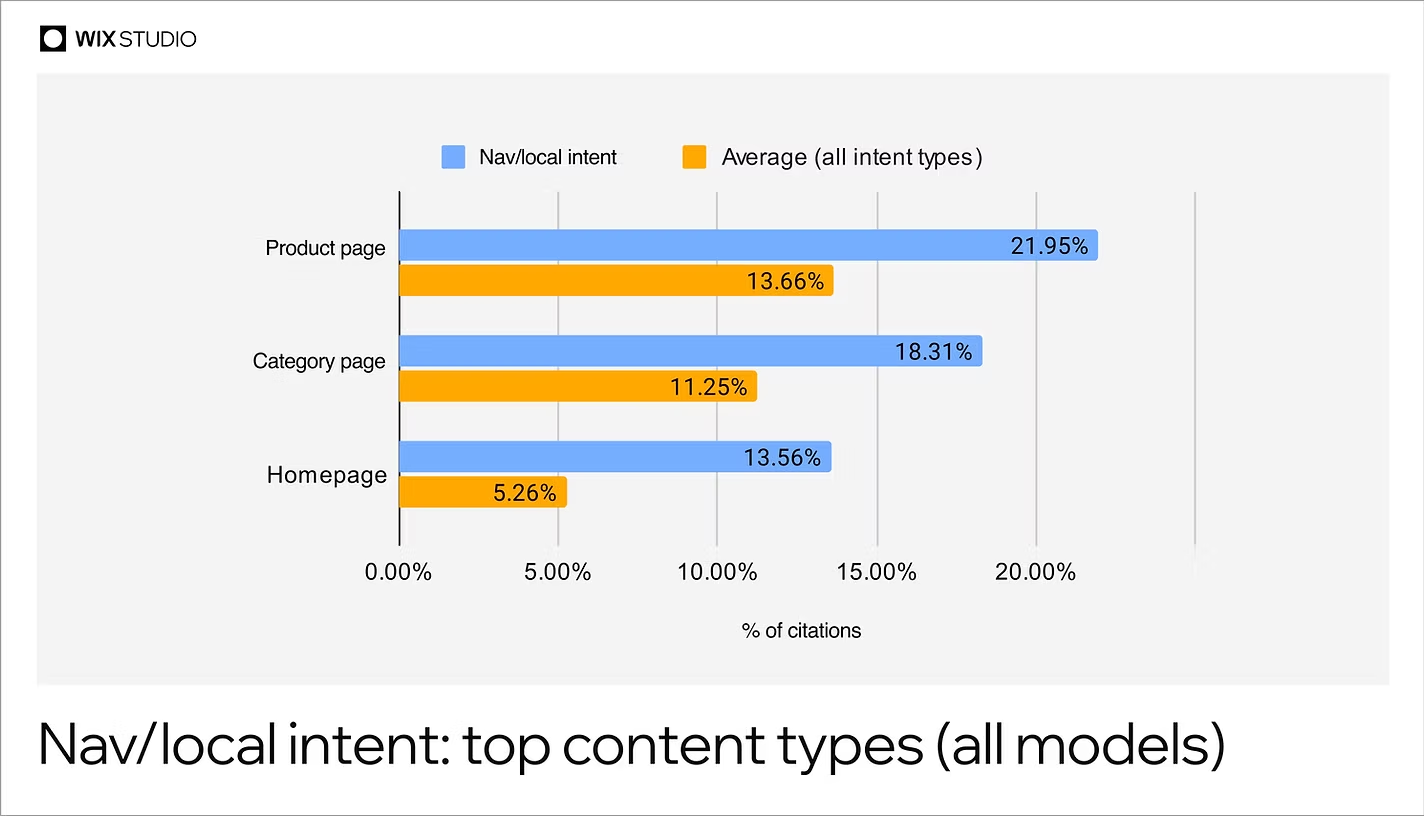

Articles captured 45.5% of citations for informational prompts, while listicles took 40.9% of commercial citations. For navigational and transactional prompts, product and category pages together accounted for roughly 40%.

The rule of thumb is shaping to be about matching the format to what the buyer is trying to do. Use articles to explain, listicles to compare, and product or category pages when the user is ready to find or buy something.

On the flip side, not every listicle carries the same weight. In the same study, Wix examined the 1,000 most-cited URLs in professional services and found that third-party listicles generated 80.9% of listicle citations, compared with 19.1% for lists where a brand placed itself first.

Although this result applies to one industry and a limited set of highly cited pages, but it still shows the advantage of appearing in independent comparisons rather than relying entirely on your own rankings.

There is also evidence that the easy listicle tactic is becoming less dependable. Seer Interactive tracked more than two million ChatGPT citations and found that citations to URLs containing “best” or “top” fell from 160,000 in December 2025 to 111,000 in January 2026—a 30% drop in absolute volume.

Their share of citations fell more modestly, from 17.2% to 15.5%, while overall citation volume also declined by 22.7%.

The study did not isolate self-promotional listicles, so it cannot prove that ChatGPT specifically penalised brands for ranking themselves first.

The safer conclusion is that format alone is not the advantage. Comparison content still works, but thin, biased rankings are fragile. Pages supported by first-hand evaluation, original research, clear methodology, and evidence have a stronger reason to be trusted and cited.

Then There’s the Reddit Problem

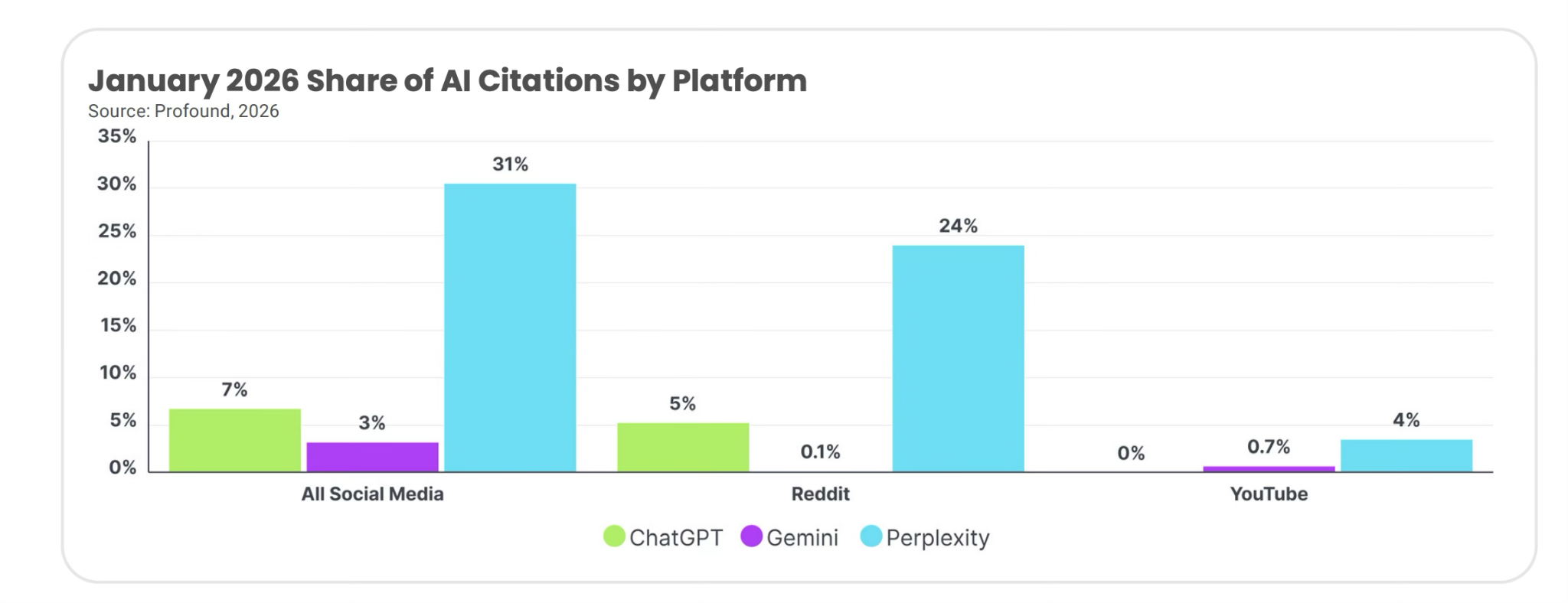

Reddit is one of the most influential and misunderstood sources in AI search. But as I’ve always maintained, its importance is not universal. It changes by engine, category, prompt, and month.

Tinuiti tracked commercial-intent prompts across nine industries and seven AI platforms, and these were the results:

- In January 2026, Reddit supplied 24% of Perplexity’s citations and more than 5% of ChatGPT’s, but only 0.1% of Gemini’s.

- By April, its share of Perplexity citations had fallen from roughly 25% in February to 7%. Reddit can dominate one engine while barely registering in another, and those patterns can change within weeks.

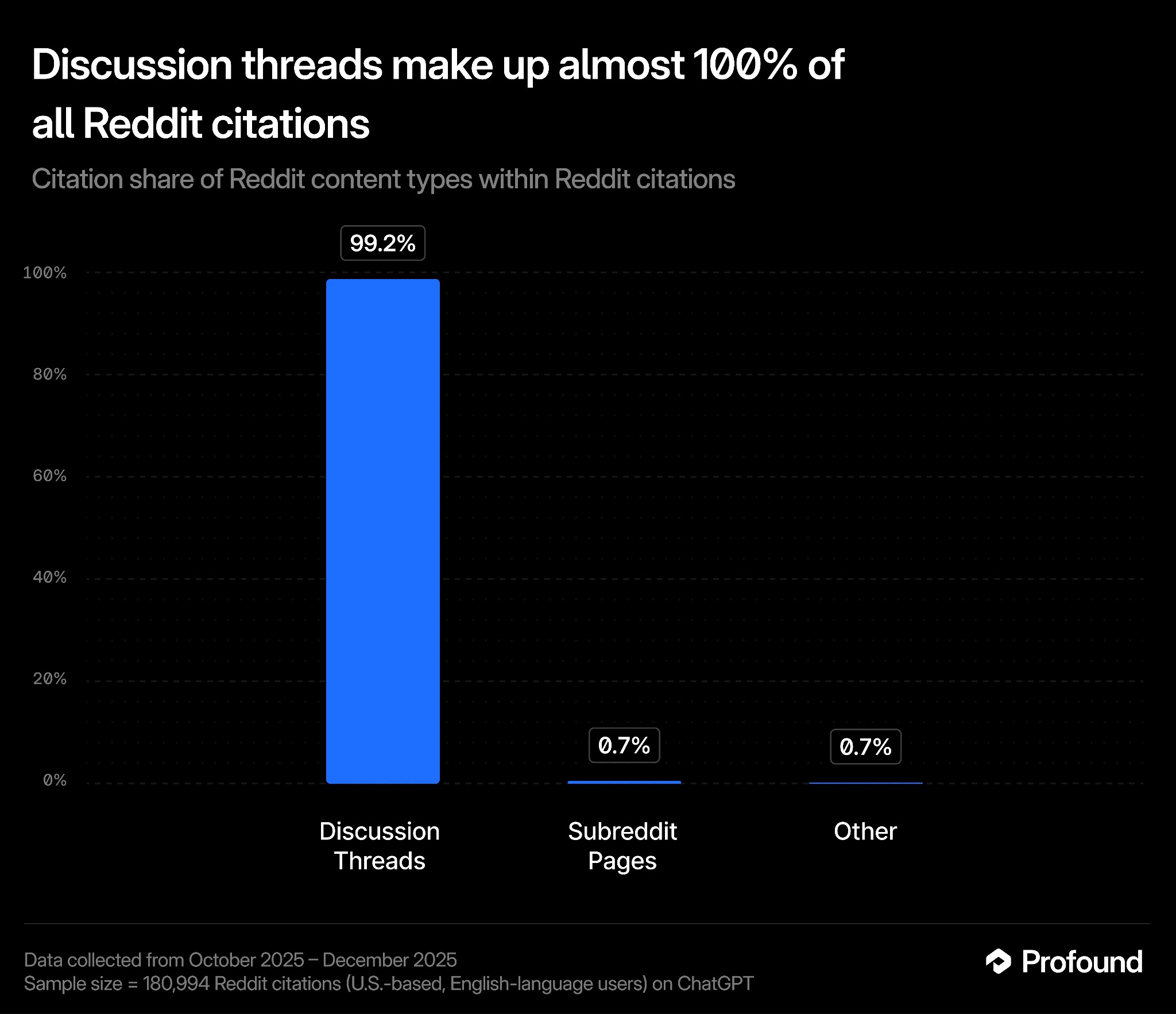

What gets cited also matters. In Profound’s analysis of ChatGPT, Reddit accounted for 2.4% of all citations, and 99% of those citations pointed to individual discussion threads rather than subreddit pages, profiles, or branded destinations.

🔖Simply creating a company account or maintaining a presence is not enough. The cited unit is usually a specific conversation that answers a specific question.

As such the response is not to ‘manufacture’ Reddit mentions. It is to identify the communities AI engines already consult for your category, monitor the conversations shaping buyer perception, answer questions genuinely, help satisfied customers share useful experiences, and correct outdated claims where possible.

Reddit is not a publishing channel a brand can control. It is a reputation layer built from conversations the brand may not have started and cannot rewrite.

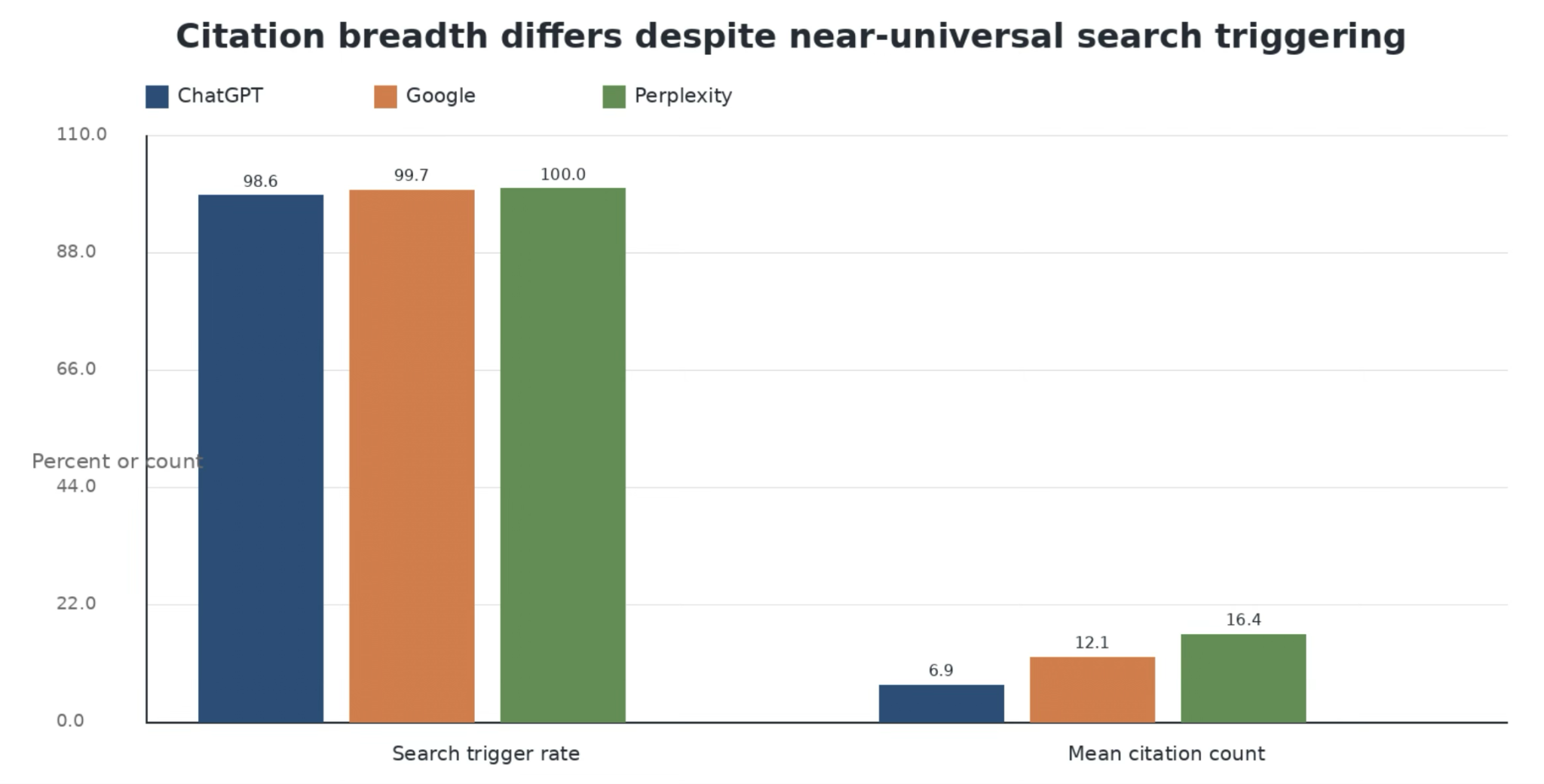

Being Cited Is Not the Same as Shaping the Answer

A final distinction runs underneath all of this and changes how a brand should value any given citation. Understand that appearing in the reference list is not the same as influencing the words of the answer, and the two can diverge just as easily.

A 2026 study analysed 602 prompts and 21,143 valid citations across ChatGPT, Google AI Overview/Gemini, and Perplexity. It separated citation selection (appearing in the source list) from; citation absorption, where a page contributes facts, language, or structure to the generated answer.

Perplexity cited an average of 16.35 sources per prompt, compared with 6.88 for ChatGPT.

But ChatGPT’s cited pages received a much higher average influence score: 0.2713, compared with 0.0646 for Perplexity. In this dataset, Perplexity spread its citations across more sources, while ChatGPT relied more heavily on the smaller set it selected.

The pages with the highest influence were not simply longer. They were more structured, more closely aligned with the answer, and richer in reusable evidence.

Pages containing statistics, definitions, comparisons, code, and procedural guidance had higher average influence than pages without them. Citations used only as general references had the lowest influence, while sources providing definitions and comparisons had the highest.

The consensus here is Perplexity cites many sources per answer but draws lightly from each, while ChatGPT cites fewer and extracts more deeply from every one. A brand can sit in Perplexity’s footnotes without touching the answer, or appear once in ChatGPT and shape two paragraphs of it.

This reframes what a citation is worth. The goal is not merely to be listed. It is to be the source the model leans on when it writes the sentence a buyer reads, and that requires earned authority to get selected plus structural clarity to get absorbed. Earned media gets you into that pool. Extractable, evidence-dense content decides whether you get quoted once you are there.

What This Means for Where You Invest

The pattern across all of this evidence points to a reallocation, and here’s how you should do it:

Move money from owned content toward earned media

If the brand’s own site accounts for something like 5 to 10% of citations while third-party coverage accounts for the rest, the budget should reflect that ratio.

The work here is public relations and analyst relations. That includes editorial placements, contributed articles, being quoted as a source in reported stories, and getting into the review platforms and category publications the engines already trust.

Publish original data, because it is the one owned asset that wins

First-party research, proprietary benchmarks, and original methodology earn citation rates several times higher than ordinary content. They also convert your domain from a self-asserting source into an evidence source the engines must reference. This is the single highest-leverage thing a brand can do on property it controls.

Map your category’s citation stack per engine

Software brands need G2 and Capterra depth; financial brands need Forbes and the personal-finance publications; B2B brands need real LinkedIn article presence.

And because the engines barely overlap, the map has to be drawn per engine, since the source that dominates Perplexity may be invisible on Gemini.

Get into neutral third-party lists rather than publishing self-serving ones

The engines increasingly discount a brand ranking itself first in its own roundup, so the effort belongs in earning inclusion in the independent comparisons that carry citation weight.

As such, you need to build an authentic community presence where your category is discussed, accepting that it is slow. Reddit and similar communities cannot be faked, which makes genuine long-term participation the only durable move.

Make everything extractable, because earned media still has to be legible

A citation gets absorbed into the answer when the page carries clear structure, definitions, numbers, and comparisons, so the content that earns authority also has to be built for machine reading.

My Thesis From The Data So Far

With the data I’ve covered here, it only makes sense to draw my conclusions and put forward two predictions on where I believe this heads next.

The earned-media premium will intensify

Because the preference is structural, rooted in how models learned credibility, improving models are likely to get better at detecting self-assertion and discounting it. This, as expected, will widen the gap between what a brand says about itself and what others say about it.

Original research becomes a crowded strategy, and the quality bar rises

As a common plague in marketing, once a method or ‘hack’ is popularized, everyone jumps in and it eventually atrophies.

As more brands discover that proprietary data is the owned asset that gets cited, the volume of published research will climb, and the engines will grow more selective about which data they treat as authoritative.